Q2 2022 Market Review

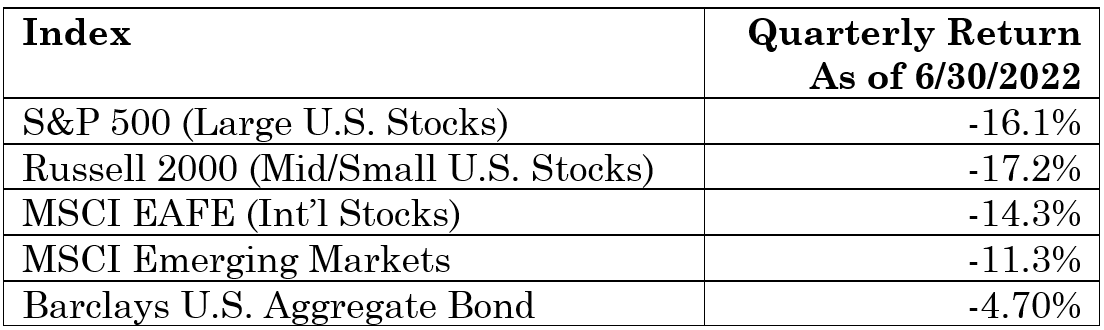

It was a brutal first half of the year for stock and bond markets across the board, as inflation remains stubbornly high and the Federal Reserve continues to raise interest rates, putting the U.S. economy at risk of a recession. The U.S. stock market entered bear market territory (a drawdown of 20% or more) in the second quarter, driven by investors’ fears of the aforementioned issues.

A Brief Overview of Bear Markets

According to Ben Carlson of Ritholtz Wealth Management and his insightful financial blog, A Wealth of Common Sense, there have been thirteen S&P 500 bear markets since World War II, and we are now in the ninth longest one.

Of course, in the middle of each, there are genuine reasons to worry that things will get worse, and it is difficult to see a path to economic growth that will lead to a stock market recovery. In early 2020, the entire world came to a grinding halt as it became apparent that Covid-19 was spreading globally. In 2008 and 2009, the U.S. housing market crumbled and financial institutions were brought to their knees. In 2000 and the years following, investors realized that technology companies’ earnings growth was not sustainable, and the re-pricing of their shares led the market lower for a painful 929 days. Yet each of these major declines was followed by a recovery to new market highs, led by unexpected successful initiatives. As long-term investors, we welcome periods of stress in the market that create a re-shuffling of favored and out-of-favor assets. This creates opportunities for the prudent investor to find value when it appears.

Notably, in 2022, as inflation and higher interest rates lead the U.S. closer to a recession, technology company stocks with very high valuations are again leading the selloff, reminiscent of the days of the early 2000’s tech bubble described above. It may serve investors well moving forward to avoid owning companies that have lofty expectations embedded in their stock prices.

In a Wall Street Journal article in May, the author analyzed various popular valuation metrics to determine whether the broad U.S. stock market (the S&P 500 index) was trading at an attractive level. Of the eight metrics (see below), not one was flashing “buy” when compared to historical levels despite the pullback in stock prices. To me, this stresses the fact that investors should avoid owning what are the most overvalued sectors in the U.S. markets (technology and healthcare), in addition to being diversified outside U.S. stock markets in international markets, where company valuations are more attractive.

Inflation Remains at the Forefront

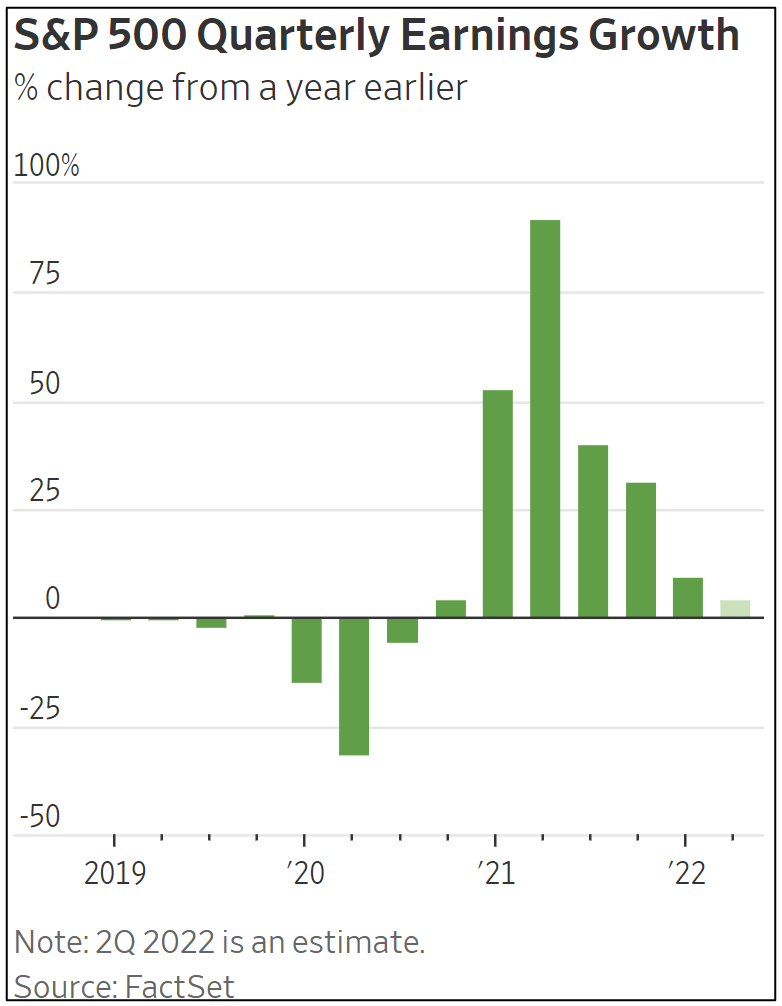

Undoubtedly, the recent market selloff has been driven by headline inflation numbers, and the Federal Reserve’s campaign to raise interest rates to combat it. Households across America are feeling the pain of record-high gas prices, and rising food & housing costs. While it remains to be seen how long these issues will continue, it is worth noting that companies are impacted by inflation as well. Quarterly earnings are slowing year-over-year for large U.S. companies as borrowing costs rise (higher interest rates), labor costs rise (wage inflation), and the cost of inputs rises (commodity price inflation).

Companies typically cope with increased costs by passing them along to consumers if possible. The Federal Reserve is now in the position of needing to cut off this vicious cycle by reducing demand for goods & services. They do this by raising borrowing costs (raising interest rates), which leads to less consumption.

For example, imagine a couple buying their first home. In the beginning of 2022, the 30-year fixed rate mortgage interest rate hovered around 3%. Their lender used their income and assets to determine that they would qualify for a $400,000 loan, which means their principal & interest payment would be $1,686 per month.

Fast forward to today, when the 30-year fixed rate mortgage is 6%, and the same couple whose income and assets allow them to afford a $1,686 monthly payment, would only be able to borrow $280,000! The impact that the Fed’s policy is having on the economy cannot be understated.

A More Positive Note

Since I have shared some of the discouraging news of what is happening in the markets, I would like to close on a more positive note. As mentioned above, unexpected successful initiatives show up and turn market sentiment positive again to begin a recovery. We do not yet know what those things will be or when they will occur, but if the past is our guide, we know they will arrive.

While I was recently lamenting the state of the market, a wise man told me, “History shows us that investing well-ahead of positive developments in the economy is rewarded.” Now is the time to take that to heart.

With you for the long haul,

Carter Ellis, CFP®

Founder

Disclosures:

Past performance is no guarantee of future success. This material is for informational use only and should not be considered investment advice.

The opinions expressed are those of Guardian Wealth Advisors, LLC. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed. Investing involves risk. Principal loss is possible.

Investment advisory services offered though Guardian Wealth Advisors, LLC D/B/A Valley Peak Financial. Guardian Wealth Advisors, LLC ("GWA") is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about GWA's investment advisory services can be found in its Form ADV Part 2, which is available upon request. GWA-22-35